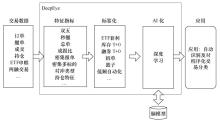

Big Data Research ›› 2018, Vol. 4 ›› Issue (5): 94-102.doi: 10.11959/j.issn.2096-0271.2018053

• APPLICATION • Previous Articles Next Articles

Guangbin XU1,Wei ZHANG2

Online:2018-09-15

Published:2018-12-10

CLC Number:

Guangbin XU, Wei ZHANG. DeepEye:a deep learning-based method of recognition and classification of program trading[J]. Big Data Research, 2018, 4(5): 94-102.

"

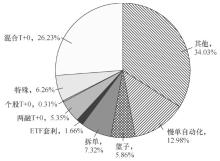

| 序号 | 类型 | 主要行为特征 |

| 1 | 篮子交易 | 满足推荐规则,有密集多标的报单 |

| 2 | 大单分拆 | 满足推荐规则,有个股密集报单 |

| 3 | 交易所交易基金 (exchange traded fund,ETF)套利 | 满足推荐规则,有相当头寸的ETF反向交易 |

| 4 | 融券T+0(日内回转交易) | 满足推荐规则,个股有相当头寸的信用买卖且无持仓 |

| 5 | 库存T+0 | 满足推荐规则,个股买卖头寸相当且有持仓 |

| 6 | 特殊账户 | 满足推荐规则,有大量订单申报但无成交的无成交账户、ETF基金账户和ETF做市商账户 |

| 7 | 混合对冲/调仓 | 满足推荐规则,整体有头寸相当的买卖 |

| 8 | 其他程序化交易 | 满足推荐规则,不属于上述分类 |

| 9 | 低频自动化 | 未达推荐规则,但持续进行低频的自动化报单 |

"

"

| 序号 | 指标 | 特征说明 |

| 1 | 日内申报5笔/s的发生次数 | 对应推荐规则 |

| 2 | 日内1 s申报并撤销的发生次数 | 对应推荐规则 |

| 3 | 日内申报笔数 | 对应推荐规则 |

| 4 | 对冲类型 | 个股对冲(1)成交个股的买卖量对冲,即|买量-卖量|/(买量+卖量)<0.1 |

| 信用交易对冲(2)不属于前一类,且|股票净买额-融券净卖额|/(股票净买额+融券净卖额)<0.1 | ||

| ETF对冲(3)不属于前两类,且|股票净买额-ETF净卖额|/(股票净买额+ETF净卖额)<0.1 | ||

| 混合对冲(4)不属于前三类,且|股票净买额-融券净卖额|/(股票净买额+融券净卖额)<0.1 | ||

| 非对冲(0)其他情况 | ||

| 5 | 成交申报比 | 成交量/申报量,无申报、显著低(<0.1)、低(0.1~0.5)、正常(>0.5) |

| 6 | 持仓多标的 | 持仓标的数量达15 |

| 7 | 个股买卖不平衡显著性 | 成交个股的|买量-卖量|/(买量+卖量),无成交、显著低(<0.1)、中(0.1~0.9)、显著高(>0.9) |

| 8 | 低频自动化特征 | 个股申报有连续60个1 min步长滑动窗口(窗口大小为2 min)内均有申报 |

| 9 | 个股密集报单 | 有个股报单笔数/s达10 笔及以上 |

| 10 | 密集多标的 | 有申报标的/s达10 只及以上 |

| 11 | 交易多标的 | 成交标的数量达10 只及以上 |

| 12 | 无/低持仓 | 无成交、无持仓或持仓量/成交量<0.1、其他 |

"

"

"

| 分类 | 准确率 | 召回率 |

| 识别 | 67% | 60% |

| 分类 | 72% | — |

| [1] | 刘逖 . 市场微观结构与交易机制设计高级指南[M]. 上海: 上海人民出版社, 2012 569-583. |

| LIU T . Market microstructure and trading mechanism advanced guideline[M]. Shanghai: Shanghai People’s PressPress, 2012: 569-583. | |

| [2] | ALDRIDGE I . High frequency trading[M]. New Jersey: John Wiley & Sons,Inc.Press, 2010: 7-35. |

| [3] | SEYFERT R . Bugs,predations or manipulations? Incompatible epistemic regimes of high-frequency trading[J]. Economy and Society, 2016,45(2): 251-277. |

| [4] | 叶伟 . 我国资本市场程序化交易的风险控制策略[J]. 证券市场导报, 2014(8): 46-52. |

| YE W . The risk control strategies of program trading of Chinese capital market[J]. Securities Market Herald, 2014(8): 46-52. | |

| [5] | 熊熊, 袁海亮, 张维 ,等. 程序化交易及其风险分析[J]. 电子科技大学学报(社科版), 2011,13(3): 32-39. |

| XIONG X , YUAN H L , ZHANG W ,et al. Program Trading overview and risk analysis[J]. Journal of University Electronics Science and Technology of China, 2011,13(3): 32-39. | |

| [6] | 彭蕾 . 中国证券市场程序化交易研究[D]. 成都:西南财经大学, 2005: 4-17. |

| PENG L . The research on pr ogram trading of the Chinese securities market[D]. Chengdu:Southwest University of Finance and Economics Press, 2005: 4-17. | |

| [7] | 陈梦根 . 算法交易的兴起及最新研究进展[J]. 证券市场导报, 2013(9): 11-17. |

| CHEN M G . Algorithmic trading's rising and advances[J]. Securities Market Herald , 2013(9): 11-17. | |

| [8] | 蓝海平 . 高频交易的技术特征、发展趋势及挑战[J]. 证券市场导报, 2014(4): 59-64. |

| LAN H P . HFT:the technique feature,developments and challenges[J]. Securities Market Herald, 2014(4): 59-64. | |

| [9] | 郭朋 . 国外高频交易的发展现状及启示[J]. 证券市场导报, 2012(7): 56-61. |

| GUO P . Development of high frequency trading and its implication[J]. Securities Market Herald, 2012(7): 56-61. | |

| [10] | YANG S Y , QIAO Q F , BELING P A ,et al. Gaussian process-based algorithmic trading strategy identification[J]. Quantitative Finance, 2015,15(10): 1683-1702. |

| [11] | QIAO Q F , BELING P A . Decision analytics and machine learning in economic and financial systems[J]. Environment Systems and Decisions, 2016,36(2): 109-113. |

| [12] | YANG S Y , QIAO Q F , BELING P A . Algorithmic trading behavior identification using reward learning method[C]// The 2014 International Joint Conference on Neural Networks,July 6-11,2014,Beijing,China. Red Hook:Curran Associates, 2014: 3807-3414. |

| [13] | 张鸿萍 . 基于时间序列交易数据的服装电商客户分类研究[J]. 现代管理, 2017,7(6): 481-492. |

| ZHANG H P . Research for customer classification of clothing E-business based on time series transaction data[J]. Modern Management, 2017,7(6): 481-492. | |

| [14] | 毛瑞, 费宇 . 基于交易数据的客户分类研究[J]. 中国证券期货, 2012(1): 22-23. |

| MAO R , FEI Y . The study of customer classification based on trading data[J]. Securities & Futures of China, 2012(1): 22-23. | |

| [15] | WANG G , ZHANG X , TANG S ,et al. Clickstream user behavior models[J]. ACM Transactions on the Web, 2017,11(4): 1-37. |

| [16] | BENSON A R , KUMAR R , TOMKINS A . Modeling user consumption sequences[C]// The 25th International Conference on World Wide Web.International World Wide Web Conferences,April 11-15,2016,Montréal,Canada. New York:ACM Press, 2016: 519-529. |

| [17] | HINTON G E , OSINDERO S , TEH Y W . A fast learning algorithm for deep belief nets[J]. Neural Computation, 2006,18(7): 1527-1554. |

| [18] | 马世龙, 乌尼日其其格, 李小平 ,等. 大数据与深度学习综述[J]. 智能系统学报, 2016,11(6): 728-742. |

| MA S L , WUNIRI Q Q G , LI X P ,et al. Deep learning with big data:state of the art and development[J]. CAAI Transactions on Intelligent Systems, 2016,11(6): 728-742. | |

| [19] | SCHMIDHUBER J . Deep learning in neural networks:an overview[J]. Neural Networks, 2015,61(1): 85-117. |

| [20] | SUTSKEVER I , VINYALS O , LE Q V . Sequence to sequence learning with neural networks[J]. Computer Science, 2014,arXiv:1409.3215. |

| [21] | 孙志远, 鲁成祥, 史忠植 ,等. 深度学习研究与进展[J]. 计算机科学, 2016,43(2): 1-8. |

| SUN Z Y , LU C X , SHI Z Z ,et al. Research and ad vances on deep learning[J]. Computer Science, 2016,43(2): 1-8. | |

| [22] | KARNOWSKI T P , AREL I , ROSE D C . Deep spatiotemporal feature learning with application to image classification[C]// The 9th International Conference on Machine Learning and Applications,December 12,2010,Washington,DC,USA. Piscataway:IEEE Computer Society, 2010: 883-888. |

| [1] | Doudou LIU, Baochen JIAO. Research on data asset cataloging of colleges and universities [J]. Big Data Research, 2023, 9(3): 71-84. |

| [2] | Yimin DENG, Xulong ZHANG, Shijing SI, Jianzong WANG, Jing XIAO. Human avatars synthesis technologies: a survey [J]. Big Data Research, 2023, 9(3): 114-139. |

| [3] | Yayun HE, Junqing PENG, Jianzong WANG, Jing XIAO. Rhythm dancer: 3D dance generation by keymotion transition graph and pose-interpolation network [J]. Big Data Research, 2023, 9(1): 23-37. |

| [4] | Yumeng CUI, Jingya WANG, Shangyi YAN, Zhizhong TAO. Automatic key information extraction of police records based on deep learning [J]. Big Data Research, 2022, 8(6): 127-142. |

| [5] | Xinhui LI, Qing SHEN, Xiongtao ZHANG. Classification algorithm for imbalance data of ECG based on PSOFS and TSK fuzzy system [J]. Big Data Research, 2022, 8(5): 139-152. |

| [6] | Zhitao ZHU, Shijing SI, Jianzong WANG, Jing XIAO. Survey on federated recommendation systems [J]. Big Data Research, 2022, 8(4): 105-132. |

| [7] | Jie WANG, Songyan ZHANG, Jiye LIANG. A semi-supervised deep learning algorithm combining consistency regularization and manifold regularization [J]. Big Data Research, 2022, 8(3): 103-114. |

| [8] | Kangting XU, Wei Song. A Chinese text sentiment analysis method combining language knowledge and deep learning [J]. Big Data Research, 2022, 8(3): 115-127. |

| [9] | Zhitao ZHAO, Lijun ZHAO, Zheng ZHANG, Ping TANG. Integration of remote sensing intelligent processing algorithm using container cloud technology [J]. Big Data Research, 2022, 8(2): 58-74. |

| [10] | Xiaolong ZHANG, Long ZHI, Jian GAO, Zhongchen MIAO, Yuefeng LIN, Yali XIANG, Yun XIONG. A semi-supervised learning financial news classification algorithm [J]. Big Data Research, 2022, 8(2): 134-144. |

| [11] | Feng ZHI, Feng TIAN, Ruofan ZHAO. Classification of big data in metrology [J]. Big Data Research, 2022, 8(1): 60-72. |

| [12] | Wen SU, Li ZHANG, Xuebing GUO, Honglin HE, Xinzhai TANG, Xiaoli REN. Classification of ecosystem long term observation data product [J]. Big Data Research, 2022, 8(1): 84-97. |

| [13] | Qiaozhuoran CAO, Zugang CHEN, Guoqing LI, Jing LI. Resource and user access control system of scientific data center [J]. Big Data Research, 2022, 8(1): 98-112. |

| [14] | Qian SUN, Yongbin QIN, Ruizhang HUANG, Lijuan LIU, Yanping CHEN. Charge prediction method combined with case elements sequence [J]. Big Data Research, 2021, 7(6): 30-40. |

| [15] | Yu ZHANG, Haibo YUAN, Yanping WANG, Shaowu DONG, Jihai ZHANG. Management control and application of the time-frequency scientific data [J]. Big Data Research, 2021, 7(6): 120-127. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||